The Real ILEC Transformation

The True Path to Open Access —

An executive from a Baby Bell once told me a Class 5 switch is essentially a billing meter. That led to a conclusion that "an ILEC is a billing system with a network built around it." It then led to a second conclusion: "It should be!"

We know the access network is the most challenging part of the network. It’s also the least profitable part of the network. Most challenging and least profitable. Doesn’t make for great cocktail party conversation, does it? Yet, it’s obviously mandatory. And to make it even more complex, consider that there are 3 separate infrastructures for voice, video, and data services.

There is good news. Your competitors, if you even have them, are in the same situation. It’s like a stalemated game of Risk. If I don’t upgrade (add armies) in that territory, then they won’t either. Or, if they upgrade there, then I’ll have to. And, if neither of us upgrade in those areas, I can upgrade elsewhere (e.g., services, content, dividends, and stock buy-backs). Best of all, if someone comes along, such as Google Fiber, we won’t let them play, or if we have to, they can play by our rules, which of course we wrote.

For now, life is good. There is manageable competition, minimal threats of a new over-builder, a favorable incumbent climate in Washington, D.C., low interest rates, etc. Yet, how different would your business environment be if a city in your territory announces a municipal-funded gigabit FTTH initiative? Or another entity announces plans to over-build your "best" areas with FTTH? These are your real threats — not the narrative that 5G will take over the world.

The Triple Play bundle has passed its economic peak. Cord cutting is becoming more than a nuisance, and is expect to continue or accelerate its steady climb. At the same time the cost for video and television content is ballooning, and due to cord cutting you must amortize your video infrastructure and content cost over fewer and fewer subscribers. Traditional voice is okay since the infrastructure is long depreciated, works fine, and a large enough segment of the population still wants it. It’s the proverbial cash cow. An issue here is millennials have never had a voice "cord to cut".

If the biggest risk to an ILEC is a new player to their game of Risk, what can the ILEC do to prevent a newcomer from destroying their business they may have spent decades to build? A key question is whether to upgrade or over-build. Then, what’s my business/financial model look like at the end. (For discussion purposes an "upgrade" would include incremental upgrades such as from GPON to XGS-PON or from ADSL to VDSL to G. fast with a "fiber a little deeper" into the network approach. An "over-build" here implies running fiber down lots of streets and connecting lots of buildings. One and done. One large construction project and be done for 25 years.)

The second aspect of a traditional transformation would be the oft noted "add new services" and do it in Cloud-like speed with this new virtual infrastructure. This is great as well. Yet voice, video/TV, and Internet access services are each challenging and costly to offer. Now add home security, home energy management, and the usual array of smart home and IoT services. Not every ILEC has the financial and technical resources, the diverse skill sets, nor scale, of an AT&T or Verizon.

The upgrade strategy doesn’t solve the cord cutting and rising video content costs problems. Strategically, an upgrade will buy you time, perhaps more than 10 years. Unless of course, communities in your footprint convince themselves that it’s a "gigabit or die" situation and do it themselves anyway. The important aspect of Community Broadband is the word community. Some communities will move forward with their own community broadband networks for reasons beyond gigabit speeds. The point to remember is an upgrade may not eliminate the gigabit over-builder threat.

Is tomorrow’s ILEC a faster version of the failing triple play bundle? There is an alternative future: Neutral Open Access. Listen to author Greg Whelan discuss this more in an exclusive ISE Podcast.

Listen Here

The Realities

The alternative is to over-build yourself. Let’s face it, the biggest challenge to over-build is capital: money. How do I fund a multi-year civil construction project based on my anticipated future cash flows? Given that this environment is transforming to Open Access worth strategic consideration? Why would an ILEC consider transitioning to Open Access? The concept itself sounds inane: let other’s service providers run on my new $millions network that took me years to build?

To properly evaluate this option, we must ensure we are talking about the same Open Access concept.

The biggest issue around Open Access is the term Open Access. I’ve come across at least 5 definitions of Open Access, some of which have failed for various reasons, and some where the use of the word open is purely gratuitous.

For example, Huntsville, Alabama, is not Open Access. Instead, it’s dark-fiber leasing or wholesaling. Great for the city, great for Google Fiber. Still not Open Access.

If an ILEC describes a town that has both Cable and Telco providers as Open Access, it is not — that is called competition.

A different version of the Open Access model is one that is forced upon their electric utility colleagues and causes instant angst amongst ILEC executives.

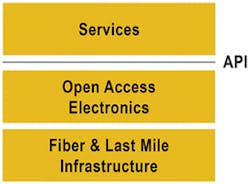

Figure 1. Three Layer Model

The real Open Access model is based on a Three Layer Model as shown in Figure 1. This model currently serves over 2 million households in Sweden and many millions more across Europe, Africa and Asia. It’s a model that is also appearing in the US, driven by forward-looking municipalities.

In today’s model, the ILEC must own and operate every function in the entire model. This is costly and requires a vast array of capabilities. The real Open Access Model identifies 3 distinct layers. Each layer is optimized based on skill sets and funding options.

Starting with the physical asset, Layer 1 is the fiber owner. That company is responsible for the design, construction, and maintenance of the passive fiber network.

Layer 2 is the entity that lights the fiber and provides the Open Access interfaces for end users, service providers, etc.

Layer 3 are service providers enabling businesses and consumers to choose from a menu of competing offers.

This is not dark-fiber leasing. In this real Open Access model, all service providers get access to customers at Layer 2 of the network protocol stack. To eliminate some confusion, the Layer 2 entity owns and operates Layer 1 and Layer 2 of the traditional Seven Layer protocol stack. So, in concept, Verizon, AT&T, and Comcast could each offer services to the same home at the same time over the same strand of fiber.

In this model, the transformed ILEC can focus on the local engineering aspects of building and maintaining a physical asset that’s hanging from poles or buried underground. Then they can decide whether to outsource the Layer 2 operations or do it themselves. The point to remember is the transformed ILEC doesn’t have to do both. The combined Open Access Layer 1 and Layer 2 in effect become true access providers; hey provide access to and from consumers, business, and service providers. That’s it.

With this model, you would no longer have to manage 3 separate infrastructures and adapt to evolving regulatory frameworks (voice, video, and data). Plus, you don’t have to deal with the worsening economics of offering traditional or linear video services.

The Open Access Transformation will enable the ILEC’s management team to focus on 2 things: 1.) providing access and 2.) satisfying the financing. With this model, the ILEC and Open Access infrastructure becomes the new billing meter. Now, that’s true transformation.

Save

Save

About the Author